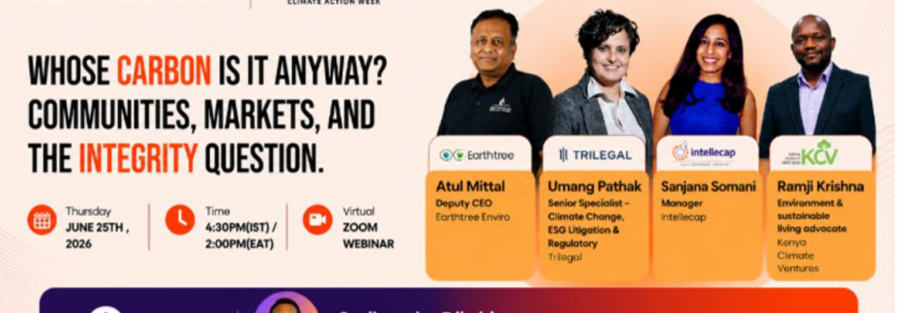

A Sankalp Dialogues panel of developers, investors, and lawyers across India and Kenya asks who carbon markets are really working for

By Vaishnavi Sinha

Walk through a farm in West Bengal or a forest plot in Meghalaya enrolled in a carbon project, and the biggest question in carbon markets isn’t answered in the methodology documents. It’s answered in whether the person who planted or protected those trees ever saw the value they created. So much of the work that defines the future of carbon markets is happening in the global south, across India and Kenya’s forests and farmlands. But after years of experience, the honest question is no longer just whether carbon markets work. The next layer is: for whom do they work? A project can check every box on paper, hit its baselines, pass its verification, and still fail the community that made it possible.

This was the question at the centre of a recent webinar bringing together a carbon project developer, an impact investor, a climate finance advisor, and a lawyer, each working at the coalface of carbon project development across India and East Africa. The panel featured Atul Mittal of Earthtree, Ramji Krishna of Kenya Climate Ventures, Sanjana Somani of Intellecap, and Umang Pathak of Trilegal. Together, they unpacked — not in theory but from lived experience — what it takes to build carbon projects where community welfare is genuinely front and centre.

The Challenge: Trust Before Technology

One of the clearest insights from the discussion was that the hardest part of developing a nature-based carbon project is not the technology, the methodology, or the financing. It is onboarding the community and creating value for them.

Atul Mittal, whose company Earthtree is currently running a large-scale ARR programme in Meghalaya, described the trust deficit that project developers routinely face. Farmers in Meghalaya have seen NGOs, government schemes, and other companies come before with promises. A carbon developer arriving with a 30 to 40 year programme falls into the same category by default.

The timing mismatch compounds the problem. For an ARR project, the first credit issuance happens at best after three years, more typically after five. Asking a landowner to hold through that window without any benefit, and on the promise of credits that may number less than projected, is what Mittal called a tolerance test. And the contract being signed is with someone who, in 40 years, will either no longer be alive or will no longer be in a decision-making position. At least two or three generational changes will occur across the life of the programme.

Earthtree’s response has been to layer in non-carbon value from the start: soil conservation, water harvesting, agricultural commodities, and agri-tourism, so that farmers see value in the trees beyond the credits. But Mittal was candid that the accountability structure of the market itself makes this harder. As he put it, accountability flows upward, from developer to registry to buyer. The landowner, the person whose land and labour underpins the entire project, is not part of that chain.

“No registry asks what happened to the community while generating the credits. I would give some part of the role to the registries to evolve.”

What Community Involvement Actually Requires

Sanjana Somani of Intellecap, drawing on her experience with carbon projects across India and East Africa including an agroforestry project in West Bengal, pushed the framing of community involvement further. It is not enough to involve communities at the design stage. They need to be continuously involved as the project evolves.

A common pattern she has observed is project developers defaulting to a benefit-sharing agreement that offers a percentage of carbon credits to farmers, and treating that as sufficient. But that is often not what communities want or what motivates them. In the West Bengal project, the more powerful incentive has been developing a value chain that takes the farmers’ products to market. That is what gives communities a sense of ownership and keeps them invested in protecting the trees.

Benefit-sharing also needs to account for costs that will inevitably rise as projects develop. Developers who do not build these costs into the design stage find that promises become difficult to keep, and that is where distrust and project failures happen.

On the question of high integrity, Somani was direct about how undefined the concept remains in practice. Institutions like the Integrity Council for the Voluntary Carbon Market (an independent body that establishes global quality standards for voluntary carbon credits) and the voluntary carbon market task force are working toward clearer parameters, and credit rating agencies are beginning to apply project-level ratings. However, there is still a lack of a fixed benchmark. A developer can establish a baseline using secondary data and call it a high integrity project. Another developer who invests in farmer-level ground data produces something meaningfully more robust, but the market does not currently distinguish between the two in a mandatory way.

“It really differs from project to project. While carbon standards ask you to have a strong baseline and strong additionality, there is no benchmark.”

What is encouraging, she noted, is that buyers are increasingly seeking high integrity projects. As long as that demand signal exists, developers will move in that direction. Moreover, methodology updates, now occurring every two years at major registries, are becoming a structural mechanism for keeping projects honest over time.

The Investor View: Legal Clarity as a Prerequisite

Ramji Krishna of Kenya Climate Ventures, which invests across waste management, water, commercial forestry, agribusiness, and renewable energy, explained that the first question KCV asks about any carbon project is not about returns. It is about ownership. Who owns the carbon, legally, socially, and commercially? If that question is unanswered, the investment risk is simply too high. Projects with unresolved ownership have been suspended, have faced legal challenge, or have become unsellable.

Kenya has seen this at significant scale. One project, once described as Africa’s largest soil carbon project, had to suspend credit generation in 2025 following legal issues in Kenyan courts over community consent. Another major player, after eleven years of operation, collapsed following a dispute with government over the volume of credits it had transferred internationally without the required letter of authorisation.

Against that backdrop, KCV’s due diligence on carbon projects goes well beyond financial modelling. It looks for documented processes, and not just evidence that a community meeting happened. It asks for the signed report, checks whether the community land management committee was democratically elected, and examines who signed the consent documents. It has seen cases where project developers formed committees that did not genuinely represent the community’s interests.

On benefit-sharing, Kenya’s 2024 Carbon Markets Regulation mandates 40% of net earnings to communities for land-based projects and 25% for non-land-based projects. But for KCV, the percentage is only part of the question. Who administers the disbursements? On what cycle? Is the process transparent? These questions matter both for protecting the community and for protecting the investor’s own reputation.

“We are not looking for projects that are simply generating carbon credits. We are looking for businesses that generate measurable impact and are able to remain commercially viable.”

KCV also requires an offtake agreement to be in place before committing capital. The investor will not enter on the hope that a buyer will emerge later.

The Legal Framework: What India Has, and What It Lacks

Umang Pathak of Trilegal situated India’s carbon market architecture within the broader regulatory landscape. India’s Carbon Credit Trading Scheme identifies nine hard-to-abate sectors that are mandated to decarbonise. Where companies in these sectors cannot close the gap through their own operations, they must buy carbon credits.

However, nature-based solutions and Agriculture, Forestry and Other Land Use (AFOLU — the land-use sector covering agriculture and forestry activities that generate or reduce greenhouse gas emissions) projects, the project types most directly involving communities and land, are not part of the main compliance market. They sit outside as offset mechanisms available to non-obligated entities. This has implications for both demand and for the level of regulatory protection applied to them.

Existing community protections in India come from other legislative frameworks: the Forest Rights Act, the Forest Conservation Act, and Panchayat legislation, all of which acknowledge the rights of indigenous communities and empower village bodies to provide consent. But these protections are not embedded in the carbon market framework itself. There is no mandatory benefit-sharing requirement written into the Carbon Credit Trading Scheme (CCTS).

“The protections are there. But if you want an enforceable right that a community member can directly invoke, you would have to use Article 21 or right to life provisions. It has not been legislated as part of the carbon market scheme.”

On CSR funds, Pathak explained that companies can legally direct CSR spending toward carbon or afforestation projects, provided those projects deliver a genuine social benefit. What they cannot do is use the same CSR funds to purchase the resulting credits for their own net zero obligations. If a company wants to use those credits, it must buy them from the community at fair market value through a separate transaction. This structure, Pathak noted, is already being used in private market deals between startups, FPOs, and corporate buyers, and the legal basis for it is sound.

DMRV: Integrity Upward, but Not Yet Downward

Atul Mittal returned to the question of digital MRV with a reframe that cut through much of the jargon that surrounds the term. DMRV, he argued, is not primarily a monitoring tool. It is a trust tool. It needs to be evaluated on whether it is enhancing integrity or simply functioning as an expensive auditory exercise.

From his experience, DMRV can address three distinct integrity problems. The first is measurement integrity: whether the carbon calculation is methodology-compliant, using satellite data, drone surveys, and canopy measurements. The second is governance integrity: whether Free, Prior and Informed Consent (FPIC) workflows are actually being followed, whether community engagement is being recorded and is verifiable. The third, which he described as emerging and as something every developer needs to start practising, is benefit-sharing integrity: whether revenue is visibly and verifiably reaching the communities it was promised to.

Earthtree’s platform includes 5-6 data layers and records the number of community meetings, secular consultations, and stakeholder engagements. But Mittal was direct about the gap that remains. DMRV today is largely a tool that works upward, providing data to registries, verifiers, and buyers. It is not yet accessible to the communities themselves.

“How far are we from a place where a landowner can log in and see how many credits have been made till now, how much benefit has come till now? I think the industry is still some distance away from that.”

India's Market and the VCM: Different Tracks, Shared Principles

Sanjana Somani offered a clear-eyed view of how India’s emerging compliance market and the voluntary carbon market relate to each other. Her view was that they are currently serving different types of participants and projects rather than competing with each other.

India’s CCTS is likely to build a pipeline of renewable energy, AWD rice, and agroforestry projects that are particularly suited to the Indian context. The global VCM, meanwhile, is shifting increasingly toward carbon removal projects: biochar, enhanced rock weathering, and direct air capture. These are distinct project categories with distinct buyer pools.

The more important point she raised is that India should be learning from the VCM’s accumulated experience rather than building its market architecture from scratch. The VCM has developed knowledge across methodology design, additionality standards, registry governance, and community safeguard principles. Incorporating those into India’s CCTS architecture would give the market a stronger foundation.

The Path Forward

The discussion did not land on a single solution. What it did surface was a set of interlocking gaps — in trust, in legal rights, in DMRV accessibility, and in project scale — that need to be addressed together if carbon markets are to deliver on their promise to communities.

Community engagement cannot be treated as a design-stage compliance step. It needs to be an ongoing relationship across the life of a project, and it needs to be built around what actually motivates communities, not just what the methodology requires.

Legal clarity around who owns the carbon and what rights communities can enforce needs to move from contractual arrangement into the market framework itself. The absence of mandatory FPIC in India’s CCTS is a gap that will create problems as the market scales.

And aggregation remains a structural barrier to investment. As Krishna noted in his closing remarks, many projects are too small to make business sense to investors individually. Finding mechanisms to aggregate related projects into investable vehicles is a precondition for attracting the kind of capital the market needs.

The technology exists. The methodologies exist. The communities are there. What is still being built is the architecture that can connect them to capital and to each other, reliably and fairly.

(Editorial note: This piece is part of the Sankalp Dialogues series, where we track emerging trends across the impact ecosystem and explore how they can be taken forward. Check the website to get involved)